China CITIC Bank International redesigned its treasury and capital markets systems to improve operating efficiency, provide stronger risk management, address current and future regulatory challenges and improve new products’ time to market.

March 12, 2018 | Neeti Aggarwal- The bank faced challenges with five different legacy systems, which lacked the pricing and flexible structuring and advanced risk management capabilities

- China CITIC Bank International implemented a large-scale redesign of its systems architecture towards a single platform over a span of two years

- With an integrated architecture, the new system facilitated treasury and market expansion, improved risk management capability, and ability to address regulations faster

China CITIC Bank International (CNCBI), a Hong Kong-based commercial bank with a network of 34 domestic branches, overseas operations in the US, Macau, Singapore and a wholly owned subsidiary for banking services in China, has treasury and markets as one of its key focus business segments. It increasingly realised the need to grow its value-added cross-border financial products business to facilitate expansion in new geographical markets. The bank aims to be a leader in RMB related products and recognised the urgent need to offer a wide range of products across all asset classes, including structured products with a faster time to market.

However, with five different legacy systems, the bank found it challenging to achieve its growth objective as it lacked the required pricing and flexible structuring capability, front-to-back systems’ consistency, and advanced risk management. In 2014, the treasury and markets business of CNCBI along with the risk, operations, finance and IT divisions, targeted a large-scale redesign of its systems architecture to address the limitations of these fragmented systems. This led to the implementation of a single platform: Murex’s MX.3 for cross-asset trading, risk, operations and finance.

The new integrated solution provides an efficient platform for financial trading, across its foreign exchange (FX) cash, interest rates, money market, fixed income, FX & interest rate derivatives and bank treasury business lines and improves the processing capacity while decreasing costs and enabling faster rollout of new products.

On the project, Michael Leung, chief information and operations officer at CNCBI commented: “As part of our bank-wide ambitious technology roadmap, the Murex project aimed at streamlining our treasury and markets business’s IT platform and make it future-proof; it now enables the business to expand into new territories, new business lines, while meeting our current and future regulatory compliance needs – all this in a timely and cost-effective way.”

This transformation meant a significant change in architecture and the project also won an award as the Best Integrated Treasury and Capital Markets Platform Implementation for 2017, under The Asian Banker Financial Markets Technology Implementation awards programme.

Patrice Meunier, Head of Hong Kong office at Murex remarked, “The project was extremely successful and we want to thank the CNCBI team and management for their strong involvement and commitment.”

The challenges

The regulatory environment is rapidly evolving and new reporting and risk compliance requirements such as Basel III and the Fundamental Review of the Trading Book (FRTB) are forcing banks to re-evaluate their risk management, reporting capabilities and underlying technology systems. The new regulatory environment brings a need for a tight integration between trading, credit and market risk, with a consistent and real-time "single version of the truth" across all departments. The wave of new regulations has triggered significant changes in market structure and is creating both threats and opportunities. Banks need the right technology in place to comply with new requirements, ranging from the comparatively simple Volcker Rule, to the more complex calculation methods for credit risk or market risk measurements.

CNCBI realised the need for a new system to meet these new demands and to optimise the costs introduced by many of these regulations, such as capital charges. It wanted to address its strategic growth needs and regulatory requirements, but it struggled with five legacy systems - Misys Summit, Calypso, MSCI RiskMetrics, GFI FENICS, ICE SuperDerivatives. The limitations of these systems and a lack of integrated architecture were hampering further business developments and caused a high cost of support and maintenance. The bank sought a platform that could provide a larger set of functions than the combination of these multiple systems, while enabling a consistent and real-time ‘single view of the truth’ to all departments.

CNCBI was looking for a solution that could:

- Improve its abilities to launch new products (across different asset classes and levels of complexity) with a faster time to market

- Automate its distribution of treasury products to its corporate clients through a product distribution platform (PDP), to increase sales turnover at lower costs

- Comply with an ever-increasing set of regulatory requirements – both the known, present ones, and the future and/or unknown ones

- Reduce the operational risks and maintenance costs by moving from a set of disparate systems for front office, operations and accounting, market risk and credit risk, towards an integrated platform

- Provide a solid foundation that enables scalability and flexibility for the bank’s transformation strategy and expanding its footprint

The solution

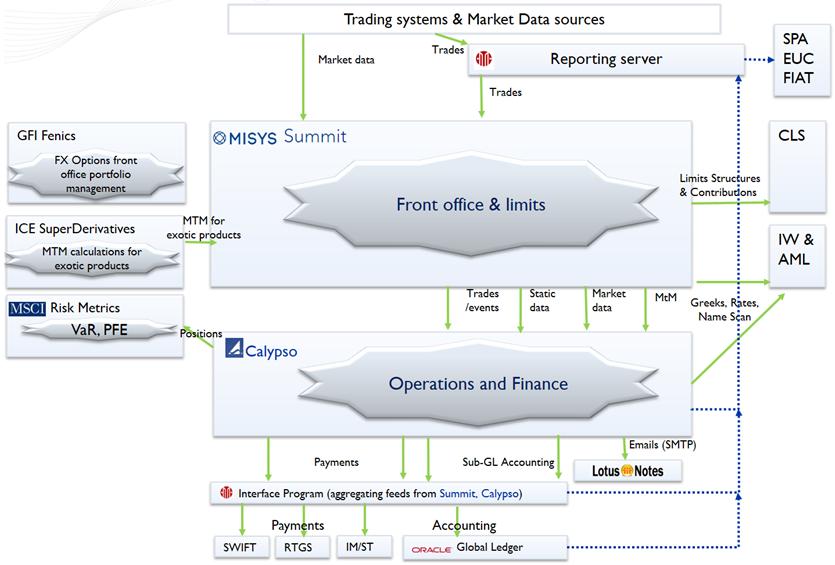

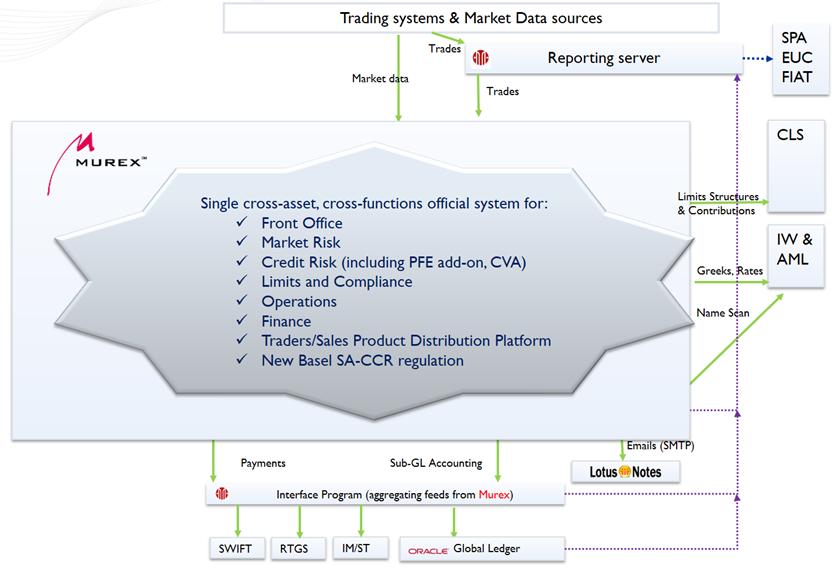

The bank explored various solutions and finally targeted a large-scale redesign of its systems architecture towards a single platform: Murex’s MX.3.The extensive scale of the project demanded a strong management commitment and execution capability. The project was implemented over a span of two years wherein the bank consolidated its five existing systems into one single front-to-back-to-risk solution (Figure 1 and Figure 2). This brought new product innovation capabilities while improving the middle office, risk and back-office functions.

The bank had fragmented legacy architecture before the project

Figure 1: Legacy architecture before implementation

Source: China CITIC Bank International

The project resulted in an integrated architecture

Figure 2: Architecture after the implementation

Source: China CITIC Bank International

With this solution, the bank now has a more efficient platform for straight-through processing of trades while providing a global consolidated view for effective management of market and credit risk. From a technology perspective Murex has simplified CNCBI treasury systems architecture, improving the service availability, stability and ongoing maintenance cost optimisation. As the new platform eliminates the inconsistencies among front, middle and back office systems it no longer needs to map interfaces and build reconciliation checks from one system to another.

The implementation

The comprehensive project was planned and implemented in two phases targeted to meet the most urgent business requirements first and to better sequence the decommissioning of legacy systems. First phase, completed in January 2016, included:

- Pricing and front office portfolio management of FX exotic and derivatives for structured products;

- Market risk measurements across all treasury and market products including Value at Risk, stress testing and sensitivities;

- PFE (Potential Future Exposure) add-on factors analytics through Monte Carlo simulation method, across all treasury and market products.

The second phase completed by November 2016, included full implementation (front to back office and finance, market risk and credit risk, limits and compliance) for FX and interest rate options and derivatives, FX cash and money markets. These features were extended to bonds, repos and other fixed income products by May 2017. During this last phase, key business initiatives were added to the project’s scope such as implementation of the PDP to improve efficiency of financial products’ price quotation and distribution to clients, and compliance with Basel III’s SA–CCR (Standard Approach for Counterparty Credit Risk) regulation. A critical component of the project was also the change management process to shift users from legacy systems to the new systems environment.

Finally, further contributing to the bank-wide ‘Rose Garden’ programme aimed at streamlining the bank’s systems, a new project was started in September 2017 to extend the Murex MX.3 platform to overseas branches in New York and Singapore, thereby replacing other legacy systems and reducing the bank’s total cost of systems’ ownership globally.

The business impact

The solution now offers CNCBI a global consolidated view to manage trading, market risk, and credit risk including PFE, CVA and Basel’s SA-CCR, while improving performance in various departments including treasury and markets, market risk and liquidity management, credit risk, and operations and finance. The new system delivered tangible benefits such as the rapid rollout of new regulatory requirements and revenue growth initiatives covering products distribution workflows from traders to sales and private banking teams.

The project allows CNCBI to simultaneously contribute to three key pillars of its strategy and long-term growth story: achieving the treasury and markets expansion plans; complying with changes in market structure and regulation; and streamlining bank’s systems.

The new system has facilitated the bank to improve its performance in the following ways:

Treasury and market expansion: With the implementation of the new system the bank was able to handle a wider range of products across all asset classes, including tailor-made structured products, to fit client’s hedge and investment needs while improving the time-to-market of these products. It provides a consistent valuation and risk engine across all functions (front office, market risk, credit risk and finance) and products, enabling generic data and analytics libraries to be extended to new products. The solution provided an efficient platform with high volume trade processing capacity and straight through processing features.

The project was designed to enable quick additions, on the same instance. For example, CNCBI will now be able to add new branches or subsidiaries with no data duplication, while leveraging on generic pricing models, facilitating faster geographic expansion and diversification into other business lines in future.

Addressing changes in market structure and regulations: Many of the new regulations such as CVA charges, SA-CCR, FRTB, IOSCO Initial Margin and Variation Margin rules, as well as IFRS9 among others cross the traditional boundaries between trading, market risk, credit risk, operations and finance.

By deploying a single platform across departments, the bank was able to address these regulations in a faster and more cost-efficient way. The new system allows the front office and risk departments to price and monitor market and credit risk in real-time through a consistent valuation and risk engine. It also improves tools for trading compliance such as stop-loss, market risk limits, real-time pre-deal credit limits checking and also enables the bank to optimise credit-related capital charges.

Improved risk management: The new system facilitates higher transparency and control on pricing models, market data sources and calibrations, and Value at Risk (VaR)/stress testing methodologies. It improves efficiency and reduces errors relating to the VaR results which are now automated, faster to calculate and available before the start of trading. This is compared to the previous systems landscape that provided VaR numbers several hours into the trading day. It also brings consistency in market data and models between front office and market risk and PFE add-on factor computation (Monte Carlo method) on a wider range of products.

The integrated project enables credit risk limits monitoring in real-time, defines more granular risk measures and takes into account netting effects and collateral mitigation effects in pre-settlement risk. The pre-settlement exposure computation for structured products has improved optimising credit risk usage: for example, for a structure made of vanilla options components such as call spread with calls and puts, the system captures the fact that credit risk exposure should be lower than the sum of components’ exposure – something that was not captured in legacy systems.

Technology efficiency: The new architecture is simpler, cheaper to maintain with a reduction in the number of interfaces, reduces the need for support teams and data duplication-related risks and skills sets. It contributes to the transformation of the bank’s worldwide systems architecture by gradually replacing legacy systems used in overseas branches.

With the new solution the bank improved its processing capacity as well as reduced costs, besides offering a global consolidated perspective to manage market risk and credit risk, improving the performance of the operations in nearly all departments of the bank, including treasury and markets, market risk and liquidity management and credit risk.

Source: Asian Banker Research

Global comparison

For effective decision making and managing risk exposures, integrated and automated treasury solutions are becoming increasingly important. Leading banks in the region are seeking greater efficiency and competitiveness with new implementations. For example, Bank of China implemented a comprehensive view of its treasury business by integrating internal and external systems that included inter system trade and transaction processing. Recently, China Merchants Bank, a leading commercial bank in China launched an enterprise-wide solution for their capital markets business to improve control over their end-to-end trading cycle from front-to-back through risk, streamline and automate their operations.

Regulations and the need for higher operational efficiencies are driving recent projects for example UBS implemented an integrated trading platform, Malaysia’s RHB consolidated its six legacy treasury systems spread across several sites and businesses into a new single global system, HDFC Bank in India streamlined its treasury IT landscape and Banca IMI recently consolidated all its front-office activities all across asset classes into one single platform. While some banks are implementing integrated projects, others are looking at modules that can be integrated with the existing systems. Some banks are also exploring cloud-based systems for higher efficiencies.

Gearing for growth

Although the overall operating environment is still full of challenges in Hong Kong, CNCBI improved its financial performance as net profit before tax increased by over 17% in 2016. As a medium-sized bank, the flexibility of CNCBI, armed with improved technology infrastructure, will enable it to react quickly to the economic changes and adapt to it in a timely manner. It is now better prepared for its growth plans of overseas expansion and a stronger market share in the capital markets and treasury business. However with evolving regulations and rapid technology developments, the bank would need to ensure it leverages emerging technologies to meet the changing strategic and customer demands.

Categories:

Keywords:Treasury, Legacy Systems, Compliance, FX, Capital Markets, Basel III, Risk Management