Wells Fargo is under scrutiny for unauthorised cross-selling and the creation of fake accounts. But was the controversy overblown?

October 23, 2016 | Research- Wells Fargo employees have been pressured by ambitious and arbitrarily set sales targets

- Financial industry continues to search for a better way in building a needs-based sales culture

- Corporate values and customer ethics are a weak force in steering front-line sales behaviour

Wells Fargo Bank is considered by many banks as a trailblazer in cross-selling, especially for knowing what it takes to succeed in this business. Commercial banks in Asia, particularly, looked up to Wells Fargo as a benchmark for best practices. However, their reputation has been tainted by recent controversies surrounding the bank.

Key executives at Wells Fargo, in particular the middle management, have coerced front-line employees into breaking rules, as the bank is obsessed in meeting aggressive sales targets. According to a report by the Wall Street Journal (WSJ), branch managers monitored employees’ progress in meeting sales targets, sometimes at a per hour basis. The sales numbers at the branch level were then reported to higher-ranking managers, which can occur as many as seven times a day, adding pressure to employees on meeting the sales targets. In return, the bank offers bonuses from $500 to $2,000 per quarter for front-line employees and $10,000 to $20,000 a year for district managers. The Los Angeles City Attorney alleged in its complaint that Wells Fargo “strictly enforced” its sales quotas with daily sales for each branch, and each sales employee, are monitored and assessed by Well Fargo’s District Managers four times a day.

Around 5,300 staff, which is one percent of the total number of employees – including front-liners, managers and senior managers – were laid-off over a five year period because of their inability to meet these expectations. However, this attrition rate is generally lower than in other banks. In competitive markets in Asia like China, Singapore and Hong Kong, there is an annual attrition rate of 15% to 20% for front-line employees. This includes laying-off underperforming employees or those that have violated audit and compliance standards.

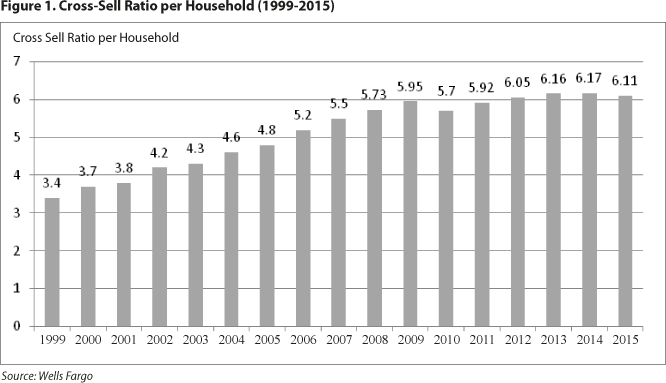

Wells Fargo increased its cross-sell ratio per household from 3.4 in 1999 to 6.11 in 2015. Nomura estimated that the cross-sell ratio would have been reduced by just 0.1 products per household had the two million unauthorised accounts never been created. The bank’s target cross-sell ratio of eight was arbitrarily set, which first appeared in its 1999 annual reporting.

Aggressive increase in cross sell ratio at Wells Fargo took place between 1999 and 2012

Wells Fargo’s problem became widespread and endemic, driven by an aggressive incentive system that was directed at front-line sales practices. Aggressive sales practices – known internally as “gaming” – emerged in the mid-2000s. Wells Fargo began its formal investigation on these practices in 2012, after findings from a third-party employee survey suggested “that employees were not comfortable with what managers were asking them to do,” according to WSJ. By 2013, the bank began restructuring its sales targets and incentive schemes to address the issue.

As a result of the case filed by the city of Los Angeles, the bank agreed to pay a total of $185 million to the Consumer Financial Protection Bureau (CFPB), the Office of the Comptroller of the Currency, and the City and County of Los Angeles for poor incentive-driven practices that included opening around two million dummy accounts to collect illegal fees from customers. Wells Fargo also announced that it will eliminate branch-level sales targets that encouraged employees to cross-sell products to customers.

Incentive Schemes

The debate on what incentive schemes should a bank implements to steer front-line employees into needs-based selling has been an old one. Regulators in countries like Hong Kong and Singapore have placed heavy restrictions on the way wealth management products are sold. Since 2008, most banks in these countries have implemented withholding or claw-back mechanisms on sales bonuses whereby employees would forfeit their bonuses when mis-selling incidences or compliance violations are detected.

When sales targets become too narrowly defined and overambitious – something that is no longer realistic based on what can be sold at the front line – sales behaviour tends to overrule corporate culture. Wells Fargo stated in its 2011 annual report that even if they sell eight products per household, they still have room to grow. They believed the average American household has the potential to grow between 14 and 16 financial services products.

To balance sales targets and to meet customer needs, banks should avoid placing quotas on cross-selling directly to customers or set cross-selling goals on branches. Banks should also avoid connecting the amount of bonuses to the number of products sold. Instead, they should take into account the overall performance including revenue and customer experience. Bonuses disbursed for meeting cross-selling targets should only be applied as part of a wider set of KPIs.

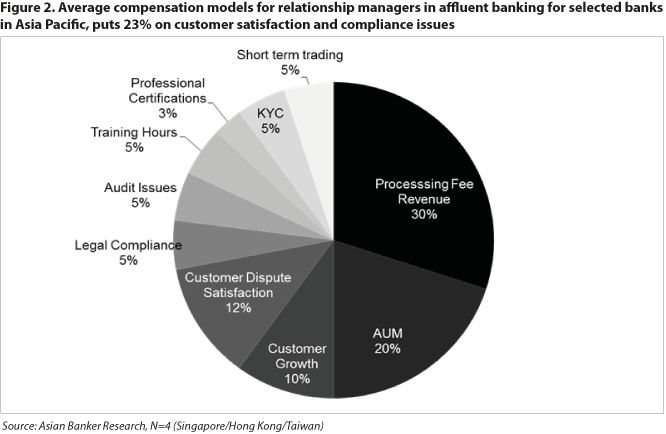

In wealth management, compensation models have moved for some large banks in Asia Pacific to a 70% (including assets under management (AUM), new clients, and revenues) to 30% (e.g. client contact ratio, satisfaction and error rates) key performance indicator (KPI) mix, with no single product selling metrics and a retainer. Customer satisfaction, compliance and audit weigh 23% in the overall mix (Figure 2).

Defining cross-selling definition and figures

Cross-selling is a tough thing to do, particularly on the branch floor. The average figures in Asia, – when mass and affluent products are combined, – have not improved much in the last few years, hovering around 1.4 sell ratio,, although it varies significantly between countries. In Singapore, the average cross- sell ratio was about 1.9 while it stood at 2.1 in Hong Kong in 2015. The cross-selling figures for the affluent segment in Asia-Pacific are around 3.0 to 5.0.

The Asian Banker measures cross-sell ratios in its annual Excellence in International Financial Services Programme, as one out of six KPIs in its sales dimension. Our methodology defines average cross-sell ratio as the number of products per individual in the mass and wealth segments (excluding private banking). Product groups are counted as one product. Cross-sell does not include ATM cards and online or mobile services.

On the other hand, bank customers in the US have around 2.71 products in their primary banks, according to data from A.T. Kearney, although savings and current accounts are counted separately. When savings and current accounts are combined, US would have an average of 1.71, faring not much better than its Asian counterparts.

Conclusion

Banks often fail to close the gap between clients’ priorities and management’s expectations of front-line staff. The issue is bigger than cross-selling alone, it is about meeting customers’ needs. More often than not, meeting customer needs are undermined by administrative tasks and excessive performance targets, thus lessening the time allotted to improve client relationship. Much must be done to calibrate this gap. John Stumpf, the CEO of Wells Fargo who recently stepped down in October, allowed its bank, managers and front-line employees to aggressively sell to its customers since the early 2000s. There is a fine balance to keep between setting sales targets and needs-based selling.

Categories:

Regulation, Retail Banking, Risk Management, Transaction BankingKeywords:Wells Fargo, CFPB, Cross-selling, Sales, Incentives